Got you, sorry, I was slow to realise this!

@avehtari Did you have any thoughts on this?

Got you, sorry, I was slow to realise this!

@avehtari Did you have any thoughts on this?

I’ve been on vacation, and now slowly going through the pile of emails. I have not thought further about this during my vacation, but I still think this is the way to do it.

I have implemented a draft solution for this in #528. Here is the updated Weibull example from above which illustrates this (plots are shown below):

## Packages ----

library(brms)

library(MASS)

library(Matrix)

### Installed from <https://github.com/fweber144/projpred/tree/cens_latent>, the

### branch for PR [#528](https://github.com/stan-dev/projpred/pull/528):

library(projpred)

###

# library(trialr)

## Simulate data ----

set.seed(1234)

### Deactivated to avoid package 'trialr':

# # Sample from LKJ distribution for a randomised correlation matrix

# cor_mat <- trialr::rlkjcorr(n = 1, K = 100, eta = 1)

###

cor_mat <- matrix(0, nrow = 100, ncol = 100)

# First and second variable sets correlate with each another within each set

cor_mat[91:95, 91:95] <- matrix(rep(0.5, times = 25), ncol = 5)

cor_mat[96:100, 96:100] <- matrix(rep(0.5, times = 25), ncol = 5)

# First and second variable sets do not correlate with one another between sets

cor_mat[91:95, 96:100] <- matrix(rep(0, times = 25))

cor_mat[96:100, 91:95] <- matrix(rep(0, times = 25))

diag(cor_mat) <- 1

# Sample some standard deviations of the variables

sd <- rgamma(100, 1, 2)

# Convert the correlation matrix to a covariance matrix

cov_mat <- diag(sd) %*% cor_mat %*% diag(sd)

# number of observations

n_obs <- 500

# Sample variables from the multivariate normal distribution

vars <- MASS::mvrnorm(

n = n_obs

,mu = rnorm(100, 30, 2.5)

,Sigma = Matrix::nearPD(cov_mat)$mat

)

# Scale the variables

scaled_vars <- apply(vars, 2, scale, scale = TRUE)

# Draws from Weibull distribution where only the last set of variables have predictive information

shape <- 1.2

predictors <- scaled_vars[,91:100] %*% rep(c(0.5, -0.5), each = 5)

linpred <- exp(0 + predictors)

scale_pred <- linpred / (gamma(1 + (1 / shape))) # brms AFT parameterisation

y <- rweibull(

n = n_obs

,shape = shape

,scale = scale_pred

)

cens <- runif(n_obs, 0, 4)

time <- pmin(y, cens)

status <- as.numeric(y <= cens)

df_sim <- data.frame(

time = time

,censored = 1 - status

,vars

)

## Fit model using 'brms' ----

# Ignore a few divergent transitions for now:

model_hs <- brm(

time | cens(censored) ~ 1 + .

,family = weibull

,data = df_sim

,prior = c(

prior(normal(0, 100), class = Intercept)

,prior(horseshoe(par_ratio = 0.1), class = b)

,prior(gamma(1, 0.5), class = shape)

)

,seed = 1234

,chains = 4

,cores = 4

,control = list(adapt_delta = 0.95, max_treedepth = 15)

,save_pars = save_pars(all = TRUE)

)

## projpred ----

### Custom extend_family() functions ----

### for Weibull family latent projection as per

### <https://mc-stan.org/projpred/articles/latent.html#negbinex>

# Needed for these custom extend_family() functions:

refm_shape <- as.matrix(model_hs)[, "shape", drop = FALSE]

### Not necessary (projpred's internal default for `latent_ilink` works

### correctly in this case):

# latent_ilink_weib <- function(

# lpreds

# ,cl_ref

# ,wdraws_ref = rep(1, length(cl_ref))

# ) {

#

# ilpreds <- exp(lpreds) # mu parameter link = "log"

# return(ilpreds)

#

# }

###

latent_ll_oscale_weib <- structure(function(

ilpreds,

dis = rep(NA, nrow(ilpreds)),

y_oscale,

wobs = rep(1, ncol(ilpreds)),

cens,

cl_ref,

wdraws_ref = rep(1, length(cl_ref))

) {

idxs_cens <- which(cens == 1)

idxs_event <- setdiff(seq_along(cens), idxs_cens)

wobs_mat <- matrix(wobs, nrow = nrow(ilpreds), ncol = ncol(ilpreds),

byrow = TRUE)

refm_shape_agg <- cl_agg(refm_shape, cl = cl_ref, wdraws = wdraws_ref)

ll_unw <- matrix(nrow = nrow(ilpreds), ncol = ncol(ilpreds))

for (idx_cens in idxs_cens) {

ll_unw[, idx_cens] <- pweibull(

y_oscale[idx_cens],

shape = refm_shape_agg,

scale = ilpreds[, idx_cens] / gamma(1 + 1 / as.vector(refm_shape_agg)),

lower.tail = FALSE,

log.p = TRUE

)

}

for (idx_event in idxs_event) {

ll_unw[, idx_event] <- dweibull(

y_oscale[idx_event],

shape = refm_shape_agg,

scale = ilpreds[, idx_event] / gamma(1 + 1 / as.vector(refm_shape_agg)),

log = TRUE

)

}

return(wobs_mat * ll_unw)

}, cens_var = ~ censored)

latent_ppd_oscale_weib <- function(

ilpreds_resamp,

dis_resamp = rep(NA, nrow(ilpreds_resamp)),

wobs = rep(1, ncol(ilpreds_resamp)),

cl_ref,

wdraws_ref = rep(1, length(cl_ref)),

idxs_prjdraws

) {

warning("The draws from this `latent_ppd_oscale` function are uncensored.")

refm_shape_agg <- cl_agg(refm_shape, cl = cl_ref, wdraws = wdraws_ref)

refm_shape_agg_resamp <- refm_shape_agg[idxs_prjdraws, , drop = FALSE]

ppd <- rweibull(

prod(dim(ilpreds_resamp)),

shape = refm_shape_agg_resamp,

scale = ilpreds_resamp / gamma(1 + 1 / as.vector(refm_shape_agg_resamp))

)

ppd <- matrix(ppd, nrow = nrow(ilpreds_resamp), ncol = ncol(ilpreds_resamp))

return(ppd)

}

### Reference model object for latent projection ----

refm_hs_weib <- get_refmodel(

model_hs

,latent = TRUE

# ,latent_ilink = latent_ilink_weib

,latent_ll_oscale = latent_ll_oscale_weib

,latent_ppd_oscale = latent_ppd_oscale_weib

)

### Variable selection ----

### For setting `parallel = TRUE` in cv_varsel() (requires

### `validate_search = TRUE`):

# ncores_cv <- 7 # change this if necessary

# doParallel::registerDoParallel(ncores_cv)

# options(projpred.export_to_workers = c("refm_shape"))

###

# For simplicity (ignoring some bad Pareto k-values for now):

refm_hs_weib_vsel_loo_valsearchF <- cv_varsel(

refm_hs_weib

,method = "forward"

,cv_method = "LOO"

,seed = 1234

,validate_search = FALSE # purely for speed

,nterms_max = 10

)

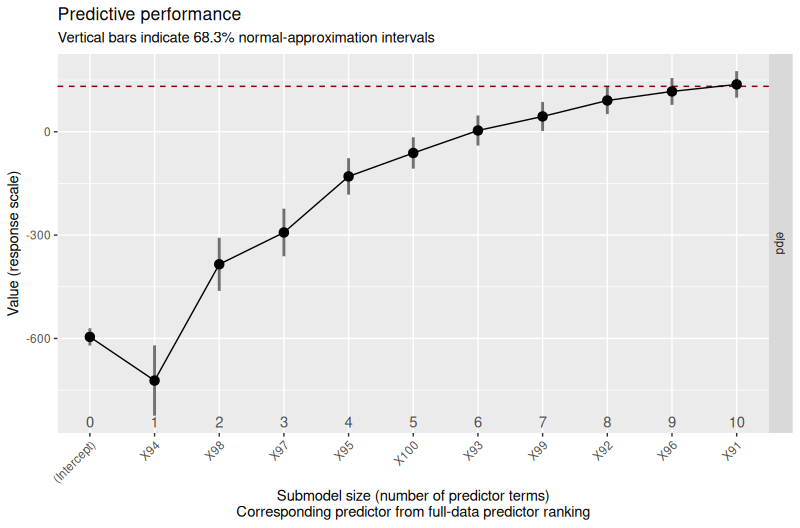

plot(refm_hs_weib_vsel_loo_valsearchF)

### If running the CV in parallel:

# # Tear down the CV parallelization setup:

# doParallel::stopImplicitCluster()

# foreach::registerDoSEQ()

###

### Final projection ----

prj <- project(

refm_hs_weib,

predictor_terms = paste0("X", 91:100)

)

### Prediction ----

prj_predict <- proj_predict(prj, .seed = 6230)

# Using the 'bayesplot' package:

library(bayesplot)

bayesplot_theme_set(ggplot2::theme_bw())

ppc_km_overlay(y = df_sim$time, yrep = prj_predict,

status_y = 1 - df_sim$censored)

The predictive performance plot produced by this code looks as follows:

The bayesplot::ppc_km_overlay() plot produced by this code looks as follows:

As you can see (by comparing this code to the code from Using {projpred} latent projection with {brms} Weibull family models - #15 by rtnliqry), I decided not to introduce any censoring-specific modification to the latent_ppd_oscale function. The reason is that the uncensored predictive distribution may already be enough (e.g., bayesplot::ppc_km_overlay() may be used for a “posterior-projection predictive check”, as illustrated here). If you really need censoring-specific modifications in the latent_ppd_oscale function, let me know.

Perhaps I’ll also add a log-normal example, but I have to see when I get the time for this.

Thanks, both, for your continued input!

Just to make sure my understanding is correct: is integrating out the censored observations in latent_ll_oscale with pweibull equivalent to what you were suggesting, @avehtari? Or was the idea to create “pseudo”-observations for the censored observations by using rweibull (left-truncated at the known censored time), and then using dweibull on these augmented times?

Yes, to be honest, I wasn’t really sure whether censoring the PPD was necessary. Presumably, by taking the censoring into account in fitting the reference model and in latent_ll_oscale, the PPD captures the uncertainty introduced by the censored observations anyway? Given that the censoring process is assumed to be random/independent of the outcome/predictors, I suppose one could at least censor predicted times that are greater than the last observed uncensored event time?

Thank you! I’m hoping the log-normal should be fairly straightforward for me to implement, assuming substituting pweibull and dweibull for plnorm and dlnorm into latent_ll_oscale as per the code above will be appropriate?