I’ve updated this now using the Weibull distribution for the prior on the residuals, and the results are much the same.

The updated Stan code:

// Y Equation

// level 1:

// y ~ normal(dy_ + ty_*TIME + cp_*X + b_*M, sigma_y)

// level 2:

// dy_ = dy + Cy*ybeta + U[id, 4] + V[roi, 4]

// ty_ = ty + U[id, 6] + V[roi, 6]

// cp_ = cp + U[id, 1] + V[roi, 1]

// b_ = b + U[id, 2] + V[roi, 2]

//

// M Equation

// level 1:

// m ~ normal(dm_ + tm_*TIME + a_*X, sigma_m)

// level 2:

// dm_ = dm + Cm*mbeta + U[id, 5] + V[roi, 5]

// tm_ = tm + U[id, 7] + V[roi, 7]

// a_ = a + U[id, 3] + V[roi, 3]

data {

int<lower=1> N; // Number of observations

int<lower=1> J; // Number of participants

int<lower=1> K; // Number of ROIs

int<lower=1> Ly; // Number of participant-varying covariates, y equation

int<lower=1> Lm; // Number of participant-varying covariates, m equation

int<lower=1,upper=J> id[N]; // Participant IDs

int<lower=1,upper=K> roi[N];// ROI ids

vector[N] X; // Treatment variable

vector[N] M; // Mediator

vector[N] Time; // Time variable (just de-trending for each J and K)

matrix[N, Ly] Cy; // participant/ROI-varying covariates, y equation - we just assume the coefficients for these do not vary by ID or ROI though the values of the variables might differ within participant by ROI, or within ROI by participant

matrix[N, Lm] Cm; // participant/ROI-varying covariates, m equation - we just assume the coefficients for these do not vary by ID or ROI though the values of the variables might differ within participant by ROI, or within ROI by participant

real prior_bs;

real prior_sigmas;

//ID Priors

real prior_id_taus;

real prior_id_lkj_shape;

//ROI Priors

real prior_roi_taus;

real prior_roi_lkj_shape;

//ID varying covars Priors

real prior_ybeta;

real prior_mbeta;

int<lower=0,upper=1> SIMULATE; //should we just simulate values?

vector[N] Y; // Continuous outcome

}

transformed data{

int<lower = 0> N_sim = 0;

int P = 7; // Number of person & ROI-varying variables: dm, dy, a,

// b, cp, ty, tm. That is, intercept for m and y

// equations, a path, b path, c prime path, and 2 time

// effects.

//This keeps us from generating a huge but empty

//vector if we're not going to put generated

//quantities in it.

if(SIMULATE == 1){

N_sim = N;

}

}

parameters{

// Regression Y on X and M

vector[P] gammas;

// 1 real dy; // Intercept

// 2 real cp; // X to Y effect

// 3 real b; // M to Y effect

// 4 real ty; // t to Y effect

// Regression M on X

// 5 real dm; // Intercept

// 6 real a; // X to M effect

// 7 real tm; // t to M effect

vector[Ly] ybeta; // ID-varying covariates to Y

vector[Lm] mbeta; // ID-varying covariates to M

real<lower=0> sigma_m;

// Correlation matrix and SDs of participant-level varying effects

cholesky_factor_corr[P] L_Omega_id;

vector<lower=0,upper=pi()/2>[P] Tau_id_unif;

// Correlation matrix and SDs of roi-level varying effects

cholesky_factor_corr[P] L_Omega_roi;

vector<lower=0,upper=pi()/2>[P] Tau_roi_unif;

// Standardized varying effects

matrix[P, J] z_U;

matrix[P, K] z_V;

real<lower=0> sigma_y;

}

transformed parameters {

//Variance scales

vector<lower=0>[P] Tau_id;

vector<lower=0>[P] Tau_roi;

// Participant-level varying effects

matrix[J, P] U;

// ROI-level varying effects

matrix[K, P] V;

// Tau_id ~ cauchy(0, prior_id_taus);

// Tau_roi ~ cauchy(0, prior_roi_taus);

for (p in 1:P) {

Tau_id[p] = prior_id_taus * tan(Tau_id_unif[p]);

Tau_roi[p] = prior_roi_taus * tan(Tau_roi_unif[p]);

}

U = (diag_pre_multiply(Tau_id, L_Omega_id) * z_U)';

V = (diag_pre_multiply(Tau_roi, L_Omega_roi) * z_V)';

}

model {

// Means of linear models

vector[N] mu_y;

vector[N] mu_m;

// Regression parameter priors

gammas ~ normal(0, prior_bs);

ybeta ~ normal(0, prior_ybeta);

mbeta ~ normal(0, prior_mbeta);

sigma_y ~ weibull(2, prior_sigmas);

sigma_m ~ weibull(2, prior_sigmas);

L_Omega_id ~ lkj_corr_cholesky(prior_id_lkj_shape);

L_Omega_roi ~ lkj_corr_cholesky(prior_roi_lkj_shape);

// Allow vectorized sampling of varying effects via stdzd z_U, z_V

to_vector(z_U) ~ normal(0, 1);

to_vector(z_V) ~ normal(0, 1);

if(SIMULATE == 0){

// Regressions

// 1 real dy; // Intercept

// 2 real cp; // X to Y effect

// 3 real b; // M to Y effect

// 4 real ty; // t to Y effect

mu_y = (gammas[2] + U[id, 2] + V[roi, 2]) .* X +

(gammas[3] + U[id, 3] + V[roi, 3]) .* M +

(gammas[4] + U[id, 4] + V[roi, 4]) .* Time +

(gammas[1] + Cy*ybeta + U[id, 1] + V[roi, 1]);

// Regression M on X

// 5 real dm; // Intercept

// 6 real a; // X to M effect

// 7 real tm; // t to M effect

mu_m = (gammas[6] + U[id, 6] + V[roi, 6]) .* X +

(gammas[7] + U[id, 7] + V[roi, 7]) .* Time +

(gammas[5] + Cm*mbeta + U[id, 5] + V[roi, 5]);

// // Data model

Y ~ normal(mu_y, sigma_y);

M ~ normal(mu_m, sigma_m);

}

}

generated quantities{

//NOTE: Include relevant generated quantities for new ROI-varying effect covariance

matrix[P, P] Omega_id; // Correlation matrix

matrix[P, P] Sigma_id; // Covariance matrix

matrix[P, P] Omega_roi; // Correlation matrix

matrix[P, P] Sigma_roi; // Covariance matrix

// Average mediation parameters

real covab_id; // a-b covariance across IDs

real corrab_id; // a-b correlation across IDs

real covab_roi; // a-b covariance acrosss ROIs

real corrab_roi; // a-b correlation acrosss ROIs

real me; // Mediated effect

real c; // Total effect

real pme; // % mediated effect

// Person-specific mediation parameters

vector[J] u_a;

vector[J] u_b;

vector[J] u_cp;

vector[J] u_dy;

vector[J] u_dm;

vector[J] u_ty;

vector[J] u_tm;

vector[J] u_c;

vector[J] u_me;

vector[J] u_pme;

// ROI-specific mediation parameters

vector[K] v_a;

vector[K] v_b;

vector[K] v_cp;

vector[K] v_dy;

vector[K] v_dm;

vector[K] v_ty;

vector[K] v_tm;

vector[K] v_c;

vector[K] v_me;

vector[K] v_pme;

// Re-named tau parameters for easy output

real dy;

real cp;

real b;

real ty;

real dm;

real a;

real tm;

real tau_id_cp;

real tau_id_b;

real tau_id_a;

real tau_id_dy;

real tau_id_dm;

real tau_id_ty;

real tau_id_tm;

real tau_roi_cp;

real tau_roi_b;

real tau_roi_a;

real tau_roi_dy;

real tau_roi_dm;

real tau_roi_ty;

real tau_roi_tm;

real Y_sim[N_sim];

real M_sim[N_sim];

// 1 u_intercept_y

// 2 u_cp (X)

// 3 u_b (M)

// 4 u_ty (Time)

// 5 u_intercept_m

// 6 u_a (X)

// 7 u_tm (Time)

tau_id_dy = Tau_id[1];

tau_id_cp = Tau_id[2];

tau_id_b = Tau_id[3];

tau_id_ty = Tau_id[4];

tau_id_dm = Tau_id[5];

tau_id_a = Tau_id[6];

tau_id_tm = Tau_id[7];

tau_roi_dy = Tau_roi[1];

tau_roi_cp = Tau_roi[2];

tau_roi_b = Tau_roi[3];

tau_roi_ty = Tau_roi[4];

tau_roi_dm = Tau_roi[5];

tau_roi_a = Tau_roi[6];

tau_roi_tm = Tau_roi[7];

Omega_id = L_Omega_id * L_Omega_id';

Sigma_id = quad_form_diag(Omega_id, Tau_id);

Omega_roi = L_Omega_roi * L_Omega_roi';

Sigma_roi = quad_form_diag(Omega_roi, Tau_roi);

//NOTE: We need to figure out what is the proper way to

// acount for covariance between a and b paths

// across both grouping factors (ID and ROI,

// crossed, not nested).

//

// I've taken a stab at something that might

// be correct but it's a very naive extension

// of the case where there is only one grouping

// factor.

covab_id = Sigma_id[6,3];

corrab_id = Omega_id[6,3];

covab_roi = Sigma_roi[6,3];

corrab_roi = Omega_roi[6,3];

// vector[P] gammas;

// // 1 real dy; // Intercept

// // 2 real cp; // X to Y effect

// // 3 real b; // M to Y effect

// // 4 real ty; // t to Y effect

// // Regression M on X

// // 5 real dm; // Intercept

// // 6 real a; // X to M effect

// // 7 real tm; // t to M effect

me = gammas[6]*gammas[3] + covab_id + covab_roi;

c = gammas[2] + me;

pme = me / c;

dy = gammas[1];

cp = gammas[2];

b = gammas[3];

ty = gammas[4];

dm = gammas[5];

a = gammas[6];

tm = gammas[7];

u_a = gammas[6] + U[, 6];

u_b = gammas[3] + U[, 3];

u_cp = gammas[2] + U[, 2];

u_dy = gammas[1] + U[, 1];

u_dm = gammas[5] + U[, 5];

u_ty = gammas[4] + U[, 4];

u_tm = gammas[7] + U[, 7];

u_me = (gammas[6] + U[, 6]) .* (gammas[3] + U[, 3]) + covab_roi; // include covariance due to the ROI grouping factor

u_c = u_cp + u_me;

u_pme = u_me ./ u_c;

v_a = gammas[6]+ V[, 6];

v_b = gammas[3]+ V[, 3];

v_cp = gammas[2] + V[, 2];

v_dy = gammas[1] + V[, 1];

v_dm = gammas[5] + V[, 5];

v_ty = gammas[4] + V[, 4];

v_tm = gammas[7] + V[, 7];

v_me = (gammas[6] + V[, 6]) .* (gammas[3] + V[, 3]) + covab_id; // include covariance due to the ROI grouping factor

v_c = v_cp + v_me;

v_pme = v_me ./ v_c;

{

vector[N] mu_y;

vector[N] mu_m;

if(SIMULATE == 1){

// Regressions

// 1 real dy; // Intercept

// 2 real cp; // X to Y effect

// 3 real b; // M to Y effect

// 4 real ty; // t to Y effect

mu_y = (gammas[2] + U[id, 2] + V[roi, 2]) .* X +

(gammas[3] + U[id, 3] + V[roi, 3]) .* M +

(gammas[4] + U[id, 4] + V[roi, 4]) .* Time +

(gammas[1] + Cy*ybeta + U[id, 1] + V[roi, 1]);

// Regression M on X

// 5 real dm; // Intercept

// 6 real a; // X to M effect

// 7 real tm; // t to M effect

mu_m = (gammas[6] + U[id, 6] + V[roi, 6]) .* X +

(gammas[7] + U[id, 7] + V[roi, 7]) .* Time +

(gammas[5] + Cm*mbeta + U[id, 5] + V[roi, 5]);

// Data model

Y_sim = normal_rng(mu_y, sigma_y);

M_sim = normal_rng(mu_m, sigma_m);

}

}

}

The prior parameters defined through the supplied data are defined:

to_fit_data$prior_bs <- 1 #normal(0,1)

to_fit_data$prior_mbeta <- 1 #normal(0,1)

to_fit_data$prior_ybeta <- 1 #normal(0,1)

to_fit_data$prior_sigmas <- 1 #weibull(2, 1);

to_fit_data$prior_id_lkj_shape <- 1 #lkj_corr_cholesky(1)

to_fit_data$prior_roi_lkj_shape <- 1 #lkj_corr_cholesky(1)

to_fit_data$prior_id_taus <- 2.5 #cauchy(0,2.5)

to_fit_data$prior_roi_taus <- 2.5 #cauchy(0,2.5)

I fit 8 chains to 8 different data sets generated by the above Stan code. Here are the diagnositc results:

- R-hat greater than 1.05: L_Omega_id[7,3], z_U[3,5]

- Exceeded wall-time (9 days)

- No issues

- R-hat greater than 1.05: gammas[1], V[2,1], V[13,1], V[16,1], u_dy[4], u_dy[6], u_dy[9], u_dy[20], u_dy[23], dy

- R-hat greater than 1.05: L_Omega_roi[5,3], V[13,3]

- No issues

- No issues

- No issues

The repository with reproducible code and output is here: https://github.com/jflournoy/mlmed_example; compiled RMarkdown document is here: https://jflournoy.github.io/mlmed_example/sim_fit_results.html.

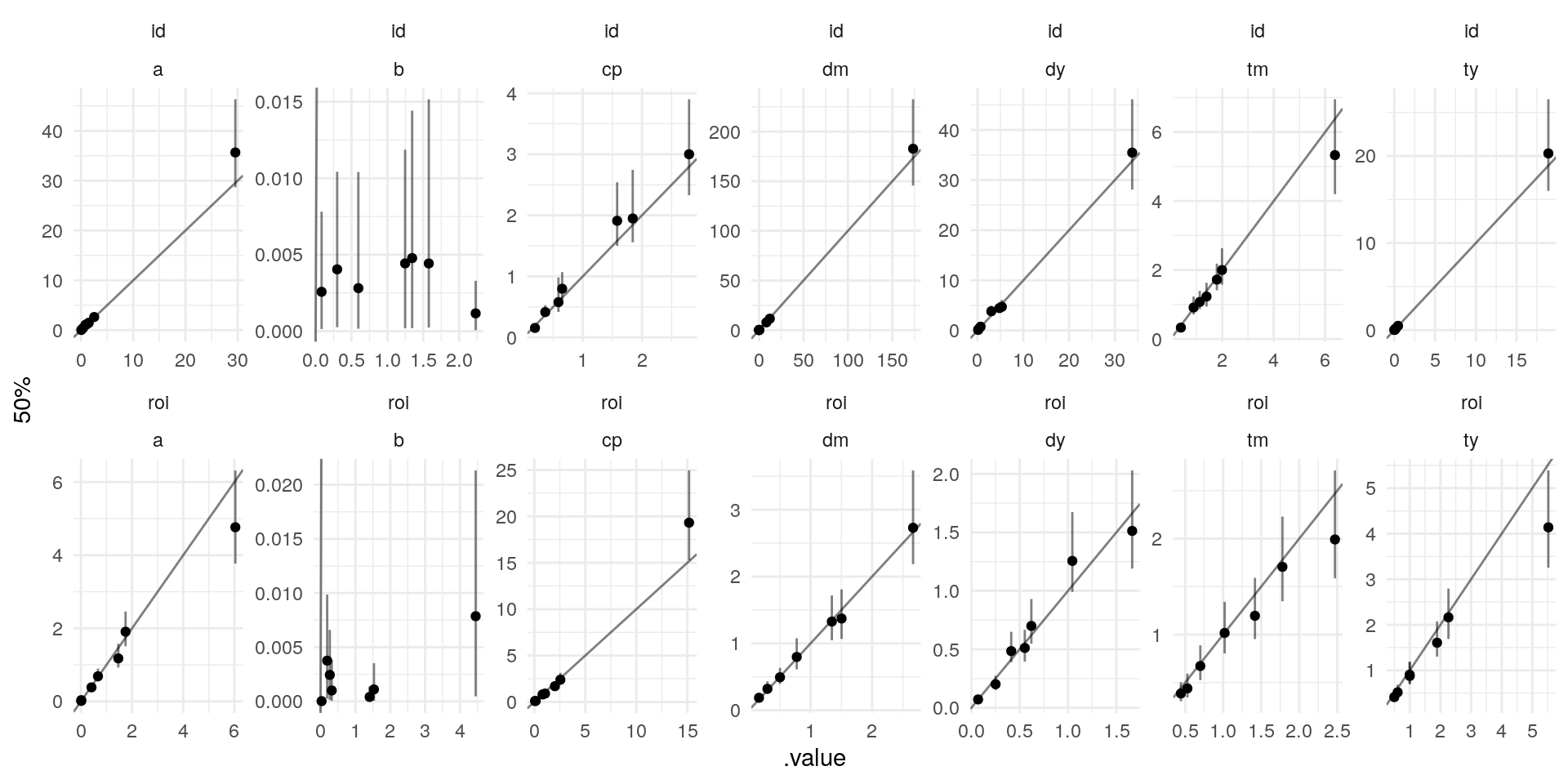

And for your convenience, the plots of the ROI-varying parameters V (they’re similar to the ID-varying U) from all 7 chains. The X axis is the generating value, and the Y axis conveys the posterior where points are medians, and lines are 95% credible intervals (and an identity line in solid black):

And plots of Tau for both V and U:

It does really look like the b parameter is consistently evincing this pathology.