I am working on a soccer model that takes in the home and away team, and outputs the sportsbook betting odds for home team winning, away team winnings, or draw. This is compositional dataset where the outcome probabilities sum to 1. I am using a hierarchical Dirichlet regression, which you can see below.

data {

int<lower=0> N; // number of rows

int<lower=0> J; // number of teams

simplex[3] y[N]; // outcome matrix

int<lower=0, upper = J> home_team[N]; // home team id

int<lower=0, upper = J> away_team[N]; // away team id

}

parameters {

vector[3] beta0; // intercepts

vector[J] beta; // beta's for each team

real<lower = 0> sigma_teams; // sigma for pooling

}

model {

vector[N] alpha1;

vector[N] alpha2;

vector[N] alpha3;

beta0[1] ~ normal(3, 2);

beta0[2] ~ normal(2, 2);

beta0[3] ~ normal(2, 2);

beta ~ normal(0, sigma_teams);

sigma_teams ~ cauchy(0, 2);

for (i in 1:N) {

alpha1[i] = exp(beta0[1] + beta[home_team[i]] + beta[away_team[i]]);

alpha2[i] = exp(beta0[2] + beta[home_team[i]] + beta[away_team[i]]);

alpha3[i] = exp(beta0[3] + beta[home_team[i]] + beta[away_team[i]]);

}

for (i in 1:N) {

y[i] ~ dirichlet([alpha1[i], alpha2[i], alpha3[i]]);

}

}

generated quantities {

simplex[3] y_rep[N]; // replicated outcomes

vector[N] alpha1;

vector[N] alpha2;

vector[N] alpha3;

[mls_bm_odds_csv.csv|attachment](upload://pGDotk696kzkqNxpKcijWBpBiZo.csv) (29.5 KB)

for (i in 1:N) {

alpha1[i] = exp(beta0[1] + beta[home_team[i]] + beta[away_team[i]]);

alpha2[i] = exp(beta0[2] + beta[home_team[i]] + beta[away_team[i]]);

alpha3[i] = exp(beta0[3] + beta[home_team[i]] + beta[away_team[i]]);

}

for (i in 1:N) {

vector[3] alpha;

alpha[1] = alpha1[i];

alpha[2] = alpha2[i];

alpha[3] = alpha3[i];

y_rep[i] = dirichlet_rng(alpha);

}

}

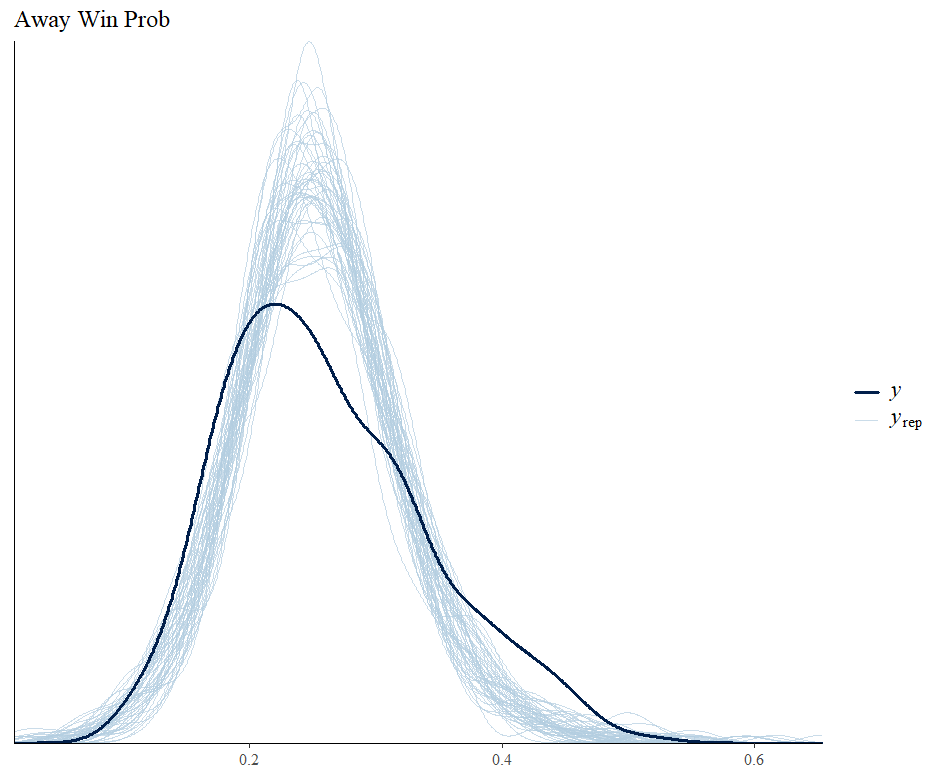

The issue is that while home and away win prob have roughly the same standard deviation, draw prob has a very tight standard deviation. I think this is what causes my posterior predictive checks to look bad.

I don’t have much experience with this type of regression, so any help would be appreciated. For reference, I added the model code and data. Thanks!

mls_implied_odds_model.R (1.7 KB)

mls_bm_odds_csv.csv (29.5 KB)